#77 - AI will fix fraud - just not how you think

Every vendor pitch I sit through these days has the same slide: “AI will solve fraud detection.”

I keep pushing back. Most of what's being sold is the wrong half of the problem.

But there is one area of fraud detection where I believe AI will actually have an immense impact.

It’s just that no one talks about it.

Regular readers know I've been banging this drum for a while: the single number that matters most in a fraud system isn't model accuracy, rule count, or even investigator experience.

It's how fast you react.

I call it the reaction cycle - the time between noticing a gap in your defenses and deploying a fix for it. Everything that matters in fraud - false positives, losses, approval rates, even customer experience - is downstream of this one number.

And AI is about to solve its most glaring issue.

Today I want to break this down in three parts: which part of the cycle is actually the bottleneck, why I believe AI will play an important part in it, and where you should absolutely not let it run unsupervised.

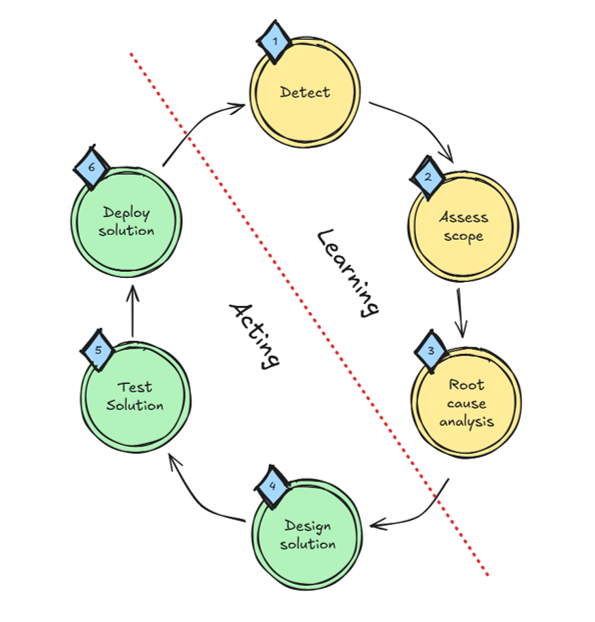

So where does the cycle actually get stuck?

The reaction cycle has six steps, across two phases.

First the learning phase: detect a gap, assess its scope, analyze its root cause. Then the acting phase: design a fix, test it, deploy it.

Most of these steps are, in principle, easy to shorten.

Better observability cuts detection time. Better processes speed up root cause analysis. Better backtesting infrastructure compresses testing.

None of this is magic - it's engineering.

But one thing refuses to cooperate.

Fresh labels.

Labels are the oxygen of every learning system - they tell it what was fraud and what wasn't. And without this oxygen, everything else falls short - alerting, scoping, analyzing, solving, and testing

Side note: I wrote about this recently in The self-learning fraud model is a lie - chargebacks arrive 30 to 90 days after the event, sometimes longer. If your system depends on them to learn, it's learning from last quarter's fraud at best.

You can buy faster detection. You can hire more analysts. You can invest in better backtests.

But you can't pay a chargeback to arrive sooner.

Or put more accurately, you can - through manual reviews - but not at scale. Right?

What changes when AI does the labeling?

AI agents can label events continuously. They review fresh data, apply the patterns they've learned, and tag events as “likely fraud” or “likely good” - without waiting for a chargeback and without needing to 50x your fraud ops team.

You might be asking: “if an AI agent can label events, why can't it just run my investigations too? Or even my real-time decisions?”

Here's the thing:

When you use AI to label for learning, you're allowed to be imperfect. No customer gets declined because an agent tagged their transaction as suspicious after the fact.

Noise in the label set is survivable - your models and rules already live with noise every day. Unreported fraud, first-party fraud, wrong rulings - labels have never been clean.

That tolerance for imperfection is the unlock.

It's what makes continuous labeling at scale possible, and I believe it's the single most important thing agentic AI does for fraud operations.

And once labels flow continuously, the rest of the cycle speeds up.

Each of the first five steps of the reaction cycle become easier with more labels, and as a result - can be executed earlier.

And that’s the mindset shift I see most folks miss - it’s not about better accuracy, it’s about increased speed.

Not how fast I can make a decision, but how fast I can learn.

So why not let AI run the whole thing?

Two reasons. One obvious, one not.

The obvious one: real-time decisioning and full investigations are a different game.

When an agent blocks a transaction or closes a case, the cost of being wrong is someone else's money or someone's frozen account.

A mistaken label sits in a dataset and gets corrected. A mistaken decline doesn't.

The stakes don't match the tolerance, and pretending otherwise is how you can inadvertently erode your customers’ trust.

But the less obvious reason is drift.

Agents learn patterns, apply them, but when the world shifts underneath them, they often don't notice - just like real humans.

Running a closed-loop automated system without supervision is how you scale tactical mistakes to strategic disasters.

And that has a concrete implication: we need a new label type in our systems.

Not just “fraud” or “good,” but “agent-labeled,” “chargeback-confirmed,” “investigator-ruled” - each tagged with its confidence profile and its lineage.

Meaning, to effectively supervise our fraud system we don’t only need the labels, but also their sources.

Without that, you simply can't run the simulations that tell you whether the agent is still doing its job.

This is the unglamorous part of the story no one will put on a slide. But it's the part that decides whether agentic labeling is the real thing or just a new way to fall behind faster.

Bottom line

I believe AI is going to fix the biggest problem in fraud detection - how fast we can learn and react to emerging threats and system breakdowns.

It’s not only about reacting to fraudsters.

It’s also about noticing data integrity issues, model drift, or even a rule release that introduced a bug to your system.

And the new balancing act fraud teams would need to master is this:

How can we learn faster while still making sure our underlying data can be trusted?

If you're already running agents somewhere in your labeling pipeline, I'd love to know: what broke first? Coverage? Drift? Auditability? Hit reply - I want to compare notes.

In the meantime, that’s all for this week.

See you next Saturday.

P.S. If you feel like you're running out of time and need some expert advice with getting your fraud strategy on track, here's how I can help you:

Free Discovery Call - Unsure where to start or have a specific need? Schedule a 15-min call with me to assess if and how I can be of value.

Schedule a Discovery Call Now »

Consultation Call - Need expert advice on fraud? Meet with me for a 1-hour consultation call to gain the clarity you need. Guaranteed.

Book a Consultation Call Now »

Fraud Strategy Action Plan - Is your Fintech struggling with balancing fraud prevention and growth? Are you thinking about adding new fraud vendors or even offering your own fraud product? Sign up for this 2-week program to get your tailored, high-ROI fraud strategy action plan so that you know exactly what to do next.

Sign-up Now »

Enjoyed this and want to read more? Sign up to my newsletter to get fresh, practical insights weekly!